🧠 The Takeaways

Today we’re building the playbook for Wayfair’s inevitable post-bankruptcy turnaround.

Curation, curation, and more curation.

Flip the biz model to focus on Airbnb hosts.

Rebrand the white labels to create Wayfair’s version of Kirkland.

+ Why you should have already started holiday planning.

LBAB! Community - Start Planning Holiday Now

If you're not planning your holiday strategy RIGHT NOW, you're already behind.

This week. Start pulling last year's performance data.

What worked. What didn't. Where we left money on the table.

Here's my holiday prep framework:

Don't get cute with your promos. Find what worked last year. Double down. Stop doing what didn't work.

Map your inventory accordingly. What are the sales trends telling you now? What tests can you run this summer/fall to gauge holiday performance?

Use smaller promotions as practice runs. Launch a new product. Test your email flows. Refine your messaging.

All of this feeds into your holiday game plan.

Mike Tyson said it best: "Everyone has a plan until they get punched in the face."

With the supply chain chaos this year, there's a massive opportunity.

If you have inventory and the big box retailers don't, you can be very aggressive on ads.

Everyone's freaking out about the economy.

That fear creates incredible sales opportunities for brands that are prepared.

Start planning now.

Let’s Examine This Biz

Note: As always, none of what follows is legal, tax, investing, financial, or any other sort of advice. And I was never here.

Wayfair, the cheap DTC furniture store, has turned into a garbage flash sale site and is staring bankruptcy in the face.

Share price: $41.24

Market Cap: $5B

L5 Performance: -76%

P/E Ratio: N/A

With $2.4B in current liabilities, only $1.8B in current assets, and a $500m net loss, Wayfair’s stuck at sea with no land in sight.

Today, we’re going to steer clear of this sinking ship since I hate the biz model and break down what will likely happen in bankruptcy court.

Financial Summary

2024 Financial Statements (YoY Comparison)

Sales: $11.9B (-1%) 😐

Gross Profits: $3.6B (-3%) 😰

OPEX: $4B (-10%) 👍

Net Income: -$492m (+33%) 😓

TLDR Analysis: Treading Water on a sinking ship

Gross Margin fell faster than Rev. 😰

Only silver lining: SG&A the biggest decrease -19% YoY 👏

Marketing +5% on a Topline -1% 😰

These %s look small, but at the scale of billions, small misses means death. Topline’s declined for 4 straight years.

They’re spending more on marketing, but it isn’t driving an increase in sales.

Opex is still >> Gross Margins.

Let’s Examine This Biz

Here are the 3 steps for whoever buys Wayfair out of bankruptcy.

1) Figure out WTH you sell

At ~12k products, Wayfair has become the “Everything on a discount store” with an absurd lack of curation.

If you scroll their HP, you get hit with a manic level of product merchandising. Deep sale on random products -> Mattresses -> Garden -> more random products -> Outdoor -> Accessories.

+ we aren’t even half way down the page yet.

Wayfair, like any retailer, has 2 jobs:

Special product curation

Unique Service offering

They are brutally failing at #1.

I don’t even need to bother getting into #2.

But here’s where rubber meets the road for a public biz with 4 years of declining sales.

They CAN’T take the right corrective action.

The obvious move here is to cut the loser categories, then cut losers (collections/products) in the remaining categories.

But the street will ruthlessly punish them if they see revenues continue to shrink. Instead, investors will bleed them dry while they tread water with a losing model.

Takeaway: ALWAYS FOCUS ON CURATION. Once you’re past 100 SKUs, cut before you add.

2) Pivot to (air)B2B.

If you want to run constant discounts, that’s fine, but you need to have an incredible CAC hack to survice.

(Wayfair doesn’t have one.)

B2B buyers, on the other hand, will spend significantly more + typically have a lower CAC as a % of Rev, because of bulk purchasing, that constant discounts do make sense for.

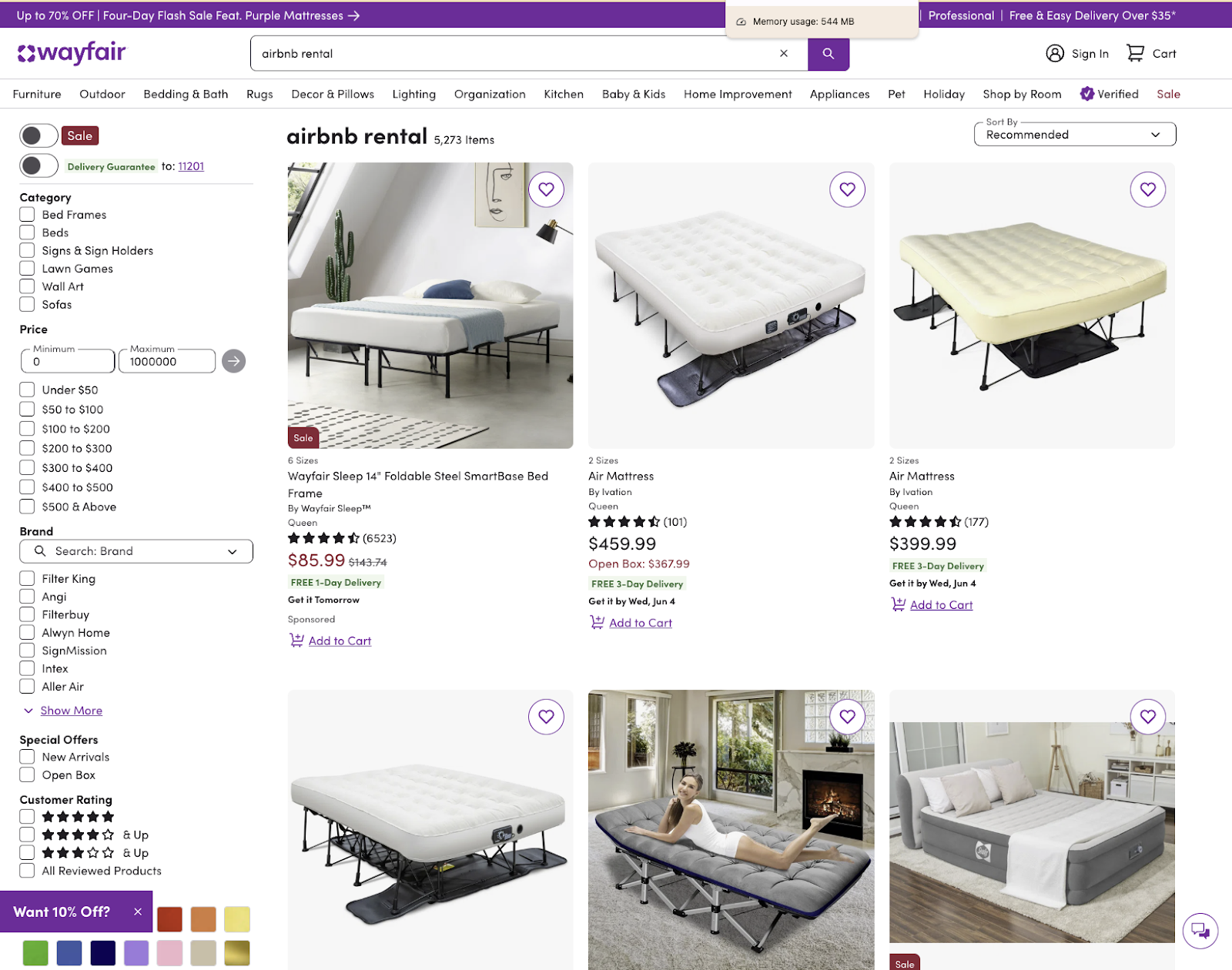

1 of the easiest entry points: Airbnb hosts.

To no one’s surprise, Wayfair is completely asleep at the wheel here.

When you search “airbnb rental” on their site, this is what comes up. 🤮

What should come up?

A full dedicated shopping experience for Airbnb hosts. Shop by house/apartment:

Size

Style

Location

Use

Amenities to rank higher on Airbnb.

There are 8m listings across 5m hosts globally, who all need to design great vacation stays to monetize their property. Furniture in vacation homes has much harder wear & tear than a normal homeowner’s = more frequent repurchase rates.

The host group would be big + spend enough that you could actually grow with them.

Takeaway: Obsess over Whales. Invest heavily.

3) Rebrand all of their white labeled products to create the Kirkland of home brands.

Wayfair is running the right strategies with terrible execution.

Over the years, they launched 4 white label brands:

Wayfair Basics - Home basics

Re/Fine - Bedding

Mercury Row - Accents + Furniture accessories.

Sand & Stable - Furniture

Here’s the problem when you become a discount diva flash sale site.

Consumers no longer trust your curation/taste and can’t figure out what’s gold vs. trash.

By having 4 separate brands with Wayfair’s “stamp of approval,” how are customers supposed to distinguish A grade products vs. another junk brand’s cheap nonsense on wayfair.com?

Amazon Essentials and Kirkland work because they slap those names on the products they want customers to know they make.

1 simple signal saying, “Trust this clone of products you love.”

Wayfair creating brands-within-the-brand that customers can only buy at Wayfair creates two headaches:

Running brands

Figuring out how to get them ranked in a marketplace.

It’s almost like they listened to 2 different consulting groups:

“Copy Amazon and create an Essentials line.”

“Mimic classic retailers and create sub brands.”

So they compromised… and did both.

Takeaway: Build 1 brand. Maximize it monetarily.

Final Thought

I will always consider Wayfair an eCom OG that proved the model for the rest of us.

But this fall from grace is brutal.

When the stock sees a temporary lift in share price because a competitor is on the verge of bankruptcy, that’s a terrible sign.

I understand Wayfair’s struggle.

They are doing well vs. their 2014 IPO.

During COVID, they swing from dead to top of the world.

Home/Outdoor got eviscerated in 2022.

But my greatest frustration is twofold:

They did more of what we’re already doing in the face of a black swan moment.

These updates to their biz don’t look like “visionary Founder” moves.

The Co-Founders are still the CEO & Co-Chairman, but the last 4 years look like they came right out of the Consultant Management playbook.

Where was getting back to their roots and reinventing their model?

Instead, they’ve been puking up new products that customers don’t want, then aggressively discounting everything.

At this point, bankruptcy is the best thing for Wayfair.

It’ll give the financial and legal structure to mine the gems and allow someone else to start over.